MediWound Might Be Exactly What Industry Giants Are Looking For After a Shock to the Market (NASDAQ: MDWD)

Medicare’s skin-substitute reset has rattled wound care, but MediWound may sit on the right side of the shock. Its late-stage biologic, EscharEx, offers differentiated upside in a category suddenly hungry for safer, drug-like assets.

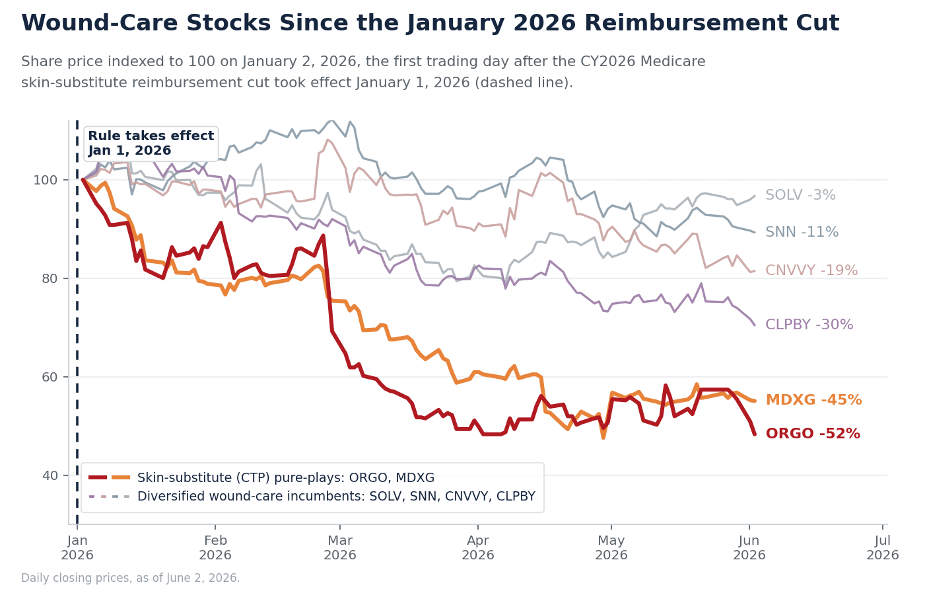

Sometimes, a major shake-up in a market can change the dynamics around which assets are considered the most valuable. In the wound-care sector, a recent substantial change in reimbursement has caused an unprecedented scale of disruption, creating a brutal repricing thus far in 2026, and setting up what may be an opportunity for under-the-radar names such as MediWound (NASDAQ: MDWD). The companies that sell skin substitutes, the cellular and tissue-based products the industry calls CTPs, have watched their shares collapse after Medicare rewrote how the category gets paid. Organogenesis (NASDAQ: ORGO) is down about 52% year to date and MiMedx (NASDAQ: MDXG) about 45%, while the S&P 500 rose roughly 11% over the same period. MediWound's lead asset sits outside the bucket that just got cut, and that distinction is the whole story.

The trigger seems to be the CY2026 Medicare Physician Fee Schedule. Starting January 1, 2026, the Centers for Medicare & Medicaid Services (CMS) reclassified skin substitutes as "incident-to" supplies rather than separately payable biologicals and moved the category to a single flat rate, a change that cuts reimbursement for many of these products by roughly 90%. The stakes are large. Medicare spending on skin substitutes had ballooned from about $256 million in 2019 to roughly $10 billion in 2024, so for companies whose revenue leaned on the old payment math, the change opens a hole almost overnight.

This is wound care's version of a pharma patent cliff. When a blockbuster drug loses exclusivity, its revenue does not erode gently, it falls off a ledge as the economics that supported it disappear, and the standard response is to go shopping, using M&A and licensing to replace the lost stream with differentiated, defensible assets. A reimbursement cliff creates similar pressure. The difference is what now counts as safe ground: not patent life, but a revenue base the CMS reset does not apply to. MediWound, whose late-stage candidate is a biologic drug rather than a skin substitute, sits on that side of the line.

Strategic buyers have already shown they will pay up for wound-care assets when they find the right one. 3M (NYSE: MMM) acquired Acelity and its KCI wound business for about $6.7 billion in 2019. Smith+Nephew (NYSE: SNN) bought substantially all the assets of Healthpoint, including its bioactive debridement franchise, for $782 million in 2012. Coloplast agreed to acquire Kerecis for up to $1.3 billion in 2023, and ConvaTec entered wound biologics through its purchase of Triad Life Sciences for up to $450 million in 2022. Together those four deals represent more than $9 billion of committed capital, and they predate the current reset that is now thinning the field of credible, differentiated targets.

That backdrop is what makes MediWound worth a closer look. Its late-stage candidate, EscharEx, is a biologic drug, the kind of differentiated, FDA-regulated asset strategic buyers may now be seeking, rather than the sort of skin substitute the reset just repriced. Here is why that matters: EscharEx is an enzymatic gel that clears the dead tissue blocking a chronic wound from healing, a process called debridement, and as a biologic drug it sits outside the category the CMS reset touches. The company is running its global Phase III VALUE trial in venous leg ulcers, with planned expansion into diabetic foot and pressure ulcers. EscharEx would enter a drug category long dominated by Smith+Nephew's Santyl, a collagenase product that reportedly generates more than $400 million a year despite first reaching the market in the 1960s, a reminder of how little pharmacologic innovation the incumbents have produced on their own.

EscharEx still has to deliver positive pivotal data and clear the FDA. But the setup seems interesting: as the reimbursement cliff forces consolidation across wound care, the assets most likely to command attention are the differentiated, de-risked ones the cut cannot touch. On that test, a late-stage drug in a category starved of innovation might be exactly the kind of asset a big player hunting for safe ground would be interested in.

Read this Next >> Broadcom's Record Quarter and the 12% Selloff: What the Market Is Really Saying About AI Chips

Recent News Highlights from MediWound

MediWound Reports First Quarter 2026 Financial Results and Provides Corporate Update

Newly Published U.S. Expert Consensus Aligns with MediWound’s Strategy for Chronic Wound Debridement

MediWound to Present New EscharEx® Data at Leading Wound Care Conferences

MediWound Reports BARDA Contract Award to Vericel for NexoBrid® Valued at up to $197 Million

Important Disclaimers and Disclosures: The author, Wall Street Wire, is a content and media technology platform that connects the market with under-the-radar companies. The platform operates a network of industry-focused media channels spanning finance, biopharma, cyber, AI, and additional sectors, delivering insights on both broader market developments and emerging or overlooked companies. Wall Street Wire is not a broker-dealer or investment adviser. References to market size estimates, valuations, price targets, or other third-party data are provided strictly for informational purposes. Wall Street Wire receives cash compensation from MediWound Ltd. (the "Issuer") for coverage and awareness services, which are provided on an ongoing subscription basis. The content above is a form of paid advertising and promotion and is for informational purposes only and does not constitute financial or investment advice. This article may contain forward-looking statements about the Issuer's products, plans, or prospects that are subject to risks and uncertainties; actual results may differ materially, and readers should review the Issuer's public filings on SEC EDGAR (sec.gov/edgar) for full risk factors. Market size figures, research estimates, or other third-party data referenced in this article are quoted from publicly available sources believed to be reliable; however, we do not independently verify or endorse them, and additional figures or estimates may exist. Full compensation details, information about the operator of Wall Street Wire, and the complete set of disclaimers and disclosures applicable to this content are available at: wallstwire.ai/disclosures. This article should not be considered an official communication of the Issuer.